Sources of Finance- Short and Long Term play a crucial role in financial management, ensuring businesses have the necessary funds for operations and growth. Short-term sources cater to immediate financial needs, while long-term sources support strategic investments and expansion. Effective management of these financial sources helps maintain liquidity, stability, and profitability.

Source of Financing

Previous Year Questions

| 2023 | Who propounded the theory of ‘Irrelevance of Capital Structure’ ? Write one keyassumption of the theory. | 2 M | |||

| 2018 | What is ‘Commercial Paper’ as an instrument for short term finance ? | 2 M | |||

| 2018 | What is the Operating Cycle Concept of Working Capital ? | 2 M | |||

| 2016 | Define non-performing assets. | 2 M | |||

| 2016 | Differentiate between Net Income Theory and Net Operating Income Theory of CapitalStructure. | 5 M | |||

| 2016 | What do you understand by Net Working Capital ? | 2 M | |||

| 2016 | What is the ‘Capital Structure’ of a company ? | 5 M | |||

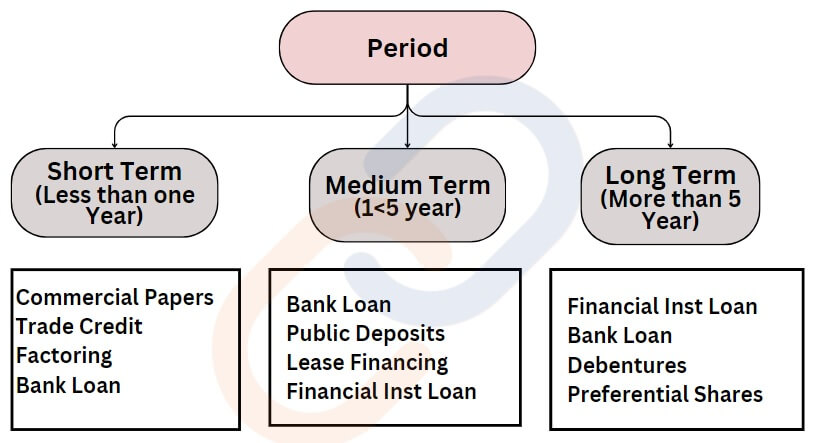

Based on period

- Short Term– Short-term funds are those which are required for a period not exceeding one year. Trade credit, loans from commercial banks and commercial papers are some of the examples of the sources that provide funds for short duration. Short term financing is most common for financing of current assets such as accounts receivable and inventories

- Medium Term-Where the funds are required for a period of more than one year but less than five years, medium-term sources of finance are used. These sources include borrowings from commercial banks, public deposits, lease financing and loans from financial institutions

- Long Term– The long-term sources fulfill the financial requirements of an enterprise for a period exceeding 5 years and include sources such as shares and debentures, long-term borrowings and loans from financial institutions. Such financing is generally required for the acquisition of fixed assets such as equipment, plant, etc

Short term sources of finance

Trade Credit

- Trade credit is a facility where suppliers allow businesses to purchase goods or services on credit without immediate payment.

- The credit period generally ranges from 30 to 90 days.

Example:

- A retailer receives stock worth ₹5 lakh from a supplier on a 60-day credit period before making payment.

Advantages:

- No interest cost.

- Improves cash flow management.

- Helps in maintaining inventory without immediate payment.

Disadvantages:

- Limited availability for new businesses with no credit history

- Delayed payments may reduce future credit limits.

Bank Overdraft

- A bank overdraft allows a business to withdraw more money than what is available in its account, up to a pre-approved limit.

- Interest is charged only on the overdrawn amount.

Example:

- A company with ₹2 lakh in its account uses an overdraft facility to withdraw ₹1 lakh extra for urgent expenses.

Advantages:

- Flexible and readily available.

- Interest is charged only on the utilized amount.

Disadvantages:

- Higher interest rates compared to loans.

- Banks may reduce or cancel overdraft limits at any time.

Short-Term Bank Loans

- Banks provide loans for a fixed short-term period (less than a year) for working capital or other immediate needs.

- Repayment is done through monthly installments or a lump sum at maturity.

Example:

- A manufacturer takes a ₹10 lakh loan for 6 months to buy raw materials.

Advantages:

- Quick funding for urgent requirements.

- Fixed repayment schedule for better planning.

Disadvantages:

- Requires collateral or a good credit history.

- Interest cost adds to business expenses.

Commercial Paper (CP)

- Commercial paper is an unsecured promissory note issued by large corporations to raise short-term funds.

- Maturity period: 7 days to 1 year.

- Issued at a discount and redeemed at face value.

Example:

- A company issues ₹50 crore worth of CPs to fund its short-term expansion.

Advantages:

- Lower interest rates than bank loans.

- No collateral required.

Disadvantages:

- Available only to large, creditworthy firms. Investors may demand high returns based on market risk.

Factoring (Accounts Receivable Financing)

- Factoring allows businesses to sell unpaid invoices (accounts receivable) to a financial institution (factor) at a discount for instant cash.

- The factor collects payments from customers later.

Example:

- A company sells ₹10 lakh worth of invoices to a factoring company for ₹9.5 lakh upfront (factor keeps ₹50,000 as fees).

Advantages:

- Immediate cash without waiting for customer payments.

- No debt burden, as it is based on receivables.

Disadvantages:

- Factoring fees reduce overall profitability.

- Loss of control over customer relationships, as the factor collects payments.

Bills Discounting (Invoice Discounting)

- Businesses sell their bills of exchange to banks or financial institutions at a discount to receive immediate cash.

- The bank collects the full payment on maturity.

Example:

- A textile exporter has a ₹5 lakh bill of exchange from a foreign buyer due in 3 months. The bank discounts it for ₹4.8 lakh, and the company gets cash upfront.

Advantages:

- Quick access to funds without waiting for bill maturity.

- No additional debt burden.

Disadvantages:

- Discounting reduces the total amount received.Only available to businesses with strong customer creditworthiness.

Working Capital Loans

- Special loans provided by banks and NBFCs to cover day-to-day business expenses like salaries, rent, and inventory purchase.

- Can be secured (against assets) or unsecured.

Example:

- A retail shop takes a ₹3 lakh working capital loan to stock up on products before the festive season.

Advantages:

- Helps maintain smooth operations.

- Flexible repayment options.

Disadvantages:

- High-interest costs if not repaid on time.

- Requires a strong financial record for approval.

Advance from Customers

- Businesses receive advance payments from customers before delivering goods or services.

- This helps fund production costs and ensures commitment from the buyer.

Example:

- A furniture manufacturer receives ₹50,000 in advance from a customer for a custom-built sofa, which will be delivered in 30 days.

Advantages:

- No interest cost – as it is a prepayment from the customer.

- Reduces reliance on external borrowing.

- Improves cash flow and working capital.

Disadvantages:

- May reduce customer trust if deliveries are delayed.

- Refunds can become an issue if orders are canceled.

Lease Financing (Short-Term Leasing)

- Instead of purchasing an asset, businesses lease (rent) equipment, vehicles, or machinery for a short duration.

- Common in industries requiring costly equipment with temporary use.

Example:

- A logistics company leases delivery trucks for six months instead of buying them.

Advantages:

- No huge upfront capital investment.

- Reduces maintenance and depreciation costs

- Helps businesses access latest technology without ownership risks.

Disadvantages:

- Total lease cost over time may be higher than purchasing.

- No ownership benefits like resale value.

Public Deposits

- Businesses raise funds by accepting deposits from the public (individual investors) for a fixed short-term period.

- The company pays interest on these deposits and repays the principal at maturity.

Example:

- A company offers 9% interest per annum for a 1-year fixed deposit of ₹1 lakh to retail investors.

Advantages:

- Easier and cheaper than bank loans.

- No dilution of ownership.

- Can be a consistent funding source if the company has a strong reputation.

Disadvantages:

- Regulatory restrictions (SEBI and RBI guidelines).

- Higher risk for investors, as deposits are unsecured.

- Available only to well-established businesses.

LONG TERM SOURCES OF FINANCE

Retained Earnings

Retained earnings refer to the portion of a company’s net profit that is not distributed as dividends but is instead reinvested back into the business for:

- Expansion

- Debt repayment

- Research and development

- Other strategic purposes

It is an essential component of shareholders’ equity and plays a crucial role in the financial growth and stability of a company.

Formula for Retained Earnings

Retained Earnings=Beginning Retained Earnings+Net Profit (or Loss)−Dividends Paid

Where:

- Beginning Retained Earnings – Retained earnings from the previous accounting period.

- Net Profit (or Loss) – The company’s earnings after deducting expenses and taxes.

- Dividends Paid – The amount distributed to shareholders as dividends.

Advantages of Retained Earnings

- No repayment obligation – Unlike loans, retained earnings do not need to be repaid.

- No interest cost – Unlike debt financing, there are no interest expenses.

- Enhances shareholder value – If reinvested wisely, retained earnings can increase a company’s overall market value.

- Strengthens financial position – Acts as a financial buffer for future uncertainties.

Disadvantages of Retained Earnings

- Opportunity cost – Shareholders might prefer receiving dividends rather than waiting for reinvested profits to yield results.

- Misuse of funds – If not managed effectively, retained earnings may be wasted on non-productive investments.

- Signaling effect – If a company retains too much earnings without distributing dividends, it may signal that the company lacks profitable investment opportunities.

Equity Shares

Equity shares, also known as ordinary shares, represent ownership in a company. Shareholders who hold equity shares are called equity shareholders, and they are considered the owners of the company. These shares give shareholders:

- The right to vote

- A share in the company’s profits (through dividends)

- Participation in decision-making during general meetings

Key Features of Equity Shares

- Voting rights – Equity shareholders have voting rights in company decisions.

- Variable dividends – Unlike preference shares, dividends are not fixed.

- Higher risk & higher returns – Potential for capital appreciation but also subject to market fluctuations.

- Last priority in liquidation – Equity shareholders are paid last after settling all debts and preference shares.

- Limited liability – Shareholders’ liability is limited to their investment amount.

Types of Equity Shares

- Ordinary Equity Shares

- The most common type of equity shares.

- Shareholders get voting rights and a share in profits.

- Dividends are variable and depend on the company’s performance.

- Bonus Shares

- Free additional shares issued to existing shareholders.

- Companies issue them from retained earnings instead of paying cash dividends.

- Rights Shares

- Offered to existing shareholders at a discounted price before being offered to the public.

- Helps companies raise additional capital while giving existing shareholders a chance to maintain their ownership percentage.

- Sweat Equity Shares

- Issued to employees or directors as a reward for their contributions to the company.

- Used to retain talented employees and encourage loyalty.

- Voting and Non-Voting Shares

- Some equity shares do not carry voting rights.

- Companies issue these to raise funds without giving control to new investors.

Advantages of Equity Shares

For the Company:

- Permanent capital – No repayment obligation like a loan.

- No interest burden – Unlike debt, companies do not have to pay interest.

- Enhances creditworthiness – A strong equity base makes it easier to raise debt.

For Investors:

- Higher returns – Potential for capital appreciation and dividend income.

- Voting rights – Gives shareholders influence in company decisions.

- Limited liability – Shareholders are not responsible for company debts beyond their investment.

Disadvantages of Equity Shares

For the Company:

- Profit sharing – More shareholders mean profits are divided among many.

- Loss of control – Issuing more equity shares dilutes ownership.

- High cost – Raising equity capital through IPOs is expensive and time-consuming.

For Investors:

- No fixed returns – Dividends are not guaranteed like interest on bonds.

- Market fluctuations – Equity share prices can be volatile.

- Last priority in liquidation – Equity shareholders get paid last if a company goes bankrupt.

How Companies Issue Equity Shares?

- Initial Public Offering (IPO)

- A company issues shares to the public for the first time to raise capital.

- Examples: Zomato, Paytm, Facebook (Meta) IPOs.

- Follow-on Public Offering (FPO)

- When an already listed company issues more shares to raise additional funds.

- Employee Stock Option Plan (ESOP)

- Companies offer shares to employees as a part of their compensation package.

Preference Shares

Preference shares (also known as preferred stock) are a type of equity that gives shareholders priority over equity shareholders in terms of dividend payments and capital repayment during liquidation. However, preference shareholders usually do not have voting rights in company decisions.

Key Features of Preference Shares

- Priority in Dividends – Preference shareholders receive dividends before equity shareholders.

- Priority in Liquidation – In case of bankruptcy, preference shareholders are repaid before equity shareholders but after debt holders.

- Fixed Dividend Rate – The dividend is usually pre-determined and fixed.

- No Voting Rights (Generally) – Unlike equity shareholders, preference shareholders do not participate in company decision-making.

Types of Preference Shares

- Cumulative and Non-Cumulative Preference Shares

- Cumulative – If dividends are unpaid in one year, they accumulate and must be paid in the future before equity shareholders get anything.

- Non-Cumulative – If a dividend is not declared in a given year, it is forfeited and not carried forward.

- Participating and Non-Participating Preference Shares

- Participating – Shareholders receive a fixed dividend plus an additional share in extra profits if the company performs well.

- Non-Participating – Shareholders only receive fixed dividends and do not share in extra profits.

- Convertible and Non-Convertible Preference Shares

- Convertible – These shares can be converted into equity shares after a certain period.

- Non-Convertible – These remain preference shares permanently.

- Redeemable and Irredeemable Preference Shares

- Redeemable – The company buys back (redeems) these shares after a fixed period.

- Irredeemable – These shares exist for the lifetime of the company and are not repurchased.

Advantages of Preference Shares

For Investors (Shareholders)

- Fixed and stable income – Investors receive guaranteed dividends, ensuring regular income.

- Lower risk than equity shares – They have priority over equity shareholders in dividends and liquidation.

- Convertible feature – Some preference shares can be converted into equity shares for potential capital growth.

- Less volatility – Preference shares are less affected by market fluctuations than equity shares.

For Companies

- Attracts conservative investors – Investors looking for fixed returns prefer preference shares.

- No additional debt burden – Unlike loans, the company does not need to repay principal amounts.

- Flexibility in dividend payments – With cumulative preference shares, the company can defer dividends in tough financial times.

Disadvantages of Preference Shares

For Investors

- Limited returns – Unlike equity shareholders, they do not benefit from increasing company profits.

- No voting rights – Investors cannot influence company decisions.

- Lower liquidity – Preference shares are not as easily tradable as equity shares.

For Companies

- Fixed dividend obligations – The company must pay dividends even in years of low profits.

- Higher cost than debt – Unlike loan interest, dividends on preference shares are not tax-deductible, making them a costly financing option.

Debentures

A debenture is a type of long-term debt instrument issued by companies and governments to raise capital. It is essentially a loan taken by an organization from investors, promising to pay interest at a fixed rate and return the principal amount at the maturity date.

Unlike secured loans, debentures are typically unsecured, meaning they do not have any specific asset backing them. Instead, they rely on the creditworthiness and reputation of the issuing entity.

Key Features of Debentures

- Fixed Interest Rate – Debenture holders receive interest at a predetermined rate, usually paid semi-annually or annually.

- Maturity Date – Debentures have a fixed tenure, after which the principal amount is repaid.

- Unsecured Nature – Most debentures are unsecured, means they do not have collateral backing them..

- No Ownership Rights – Unlike shareholders, debenture holders do not get ownership or voting rights in the company.

- Priority in Liquidation – If a company goes bankrupt, debenture holders are paid before shareholders but after secured creditors.

Types of Debentures

Based on Security

- Secured Debentures – Backed by the company’s assets as collateral.

- Unsecured Debentures – Not backed by any specific asset, relying only on the issuer’s creditworthiness.

Based on Convertibility

- Convertible Debentures – Can be converted into equity shares after a certain period.

- Non-Convertible Debentures (NCDs) – Cannot be converted into shares and only provide fixed interest.

Based on Redeemability

- Redeemable Debentures – Have a fixed maturity date when the principal is repaid.

- Irredeemable (Perpetual) Debentures – Do not have a fixed repayment date; the company repays them at its discretion.

Based on Registration

- Registered Debentures – Issued in the name of a specific investor, and ownership is recorded in the company’s books.

- Bearer Debentures – Not registered in the investor’s name; whoever holds them is considered the owner.

Based on Interest Payment

- Fixed-Rate Debentures – Carry a predetermined interest rate.

- Floating-Rate Debentures – Interest rates vary based on market conditions.

Advantages of Debentures

- Steady Income – Investors receive fixed interest payments regularly.

- Lower Risk – Compared to equity investments, debentures have lower risk due to fixed returns.

- Priority in Repayment – Debenture holders are repaid before equity shareholders in case of liquidation.

- No Ownership Dilution – Companies can raise funds without giving up ownership or control.

Disadvantages of Debentures

- Interest Obligation – Companies must pay interest even in financial distress, unlike dividends that are optional.

- Repayment Burden – At maturity, the company must repay the principal, which can create financial stress.

- Inflation Risk – Fixed interest rates may not keep up with inflation, reducing real returns for investors.

Long-term loan

A long-term loan is a type of debt financing in which a borrower receives a large sum of money upfront and agrees to repay it over an extended period through regular installments. These loans can be secured (with collateral) or unsecured (based on creditworthiness).

Long-term loans are mainly used for:

- Business expansion and asset purchase

- Infrastructure development (factories, highways, power plants)

- Real estate financing (home loans, commercial property loans)

- Education and personal development loans

Characteristics of Long-Term Loans

- Extended Repayment Period – Usually more than one year, often ranging from 5 to 30 years.

- Large Loan Amount – Suitable for capital investments, infrastructure, and major business projects.

- Fixed or Floating Interest Rates – Borrowers can choose between:

- Fixed-rate loans (constant interest throughout the term)

- Floating-rate loans (interest fluctuates with market rates)

- Collateral Requirement – Many loans require assets (property, equipment, or stock) as security.

- Structured Repayment Schedule – Monthly, quarterly, or yearly payments based on an agreed schedule.

- Specific Purpose Funding – Used for business growth, real estate and development projects.

Sources of Long-Term Loans

- Commercial Banks – Provide loans to businesses, individuals, and governments.

- Development Banks – Offer long-term project financing (e.g., World Bank, Asian Development Bank).

- Non-Banking Financial Companies (NBFCs) – Provide flexible business and personal loans.

- Government Schemes – Offer subsidized loans for startups, businesses, and farmers.

Advantages of Long-Term Loans

- Availability of Large Capital – Helps businesses and individuals fund high-value investments without immediate financial strain.

- Flexible Repayment Period – Repayment is spread over years or decades, reducing monthly financial burden.

- Lower Interest Rates – Compared to short-term loans, long-term loans often have lower interest rates.

- Encourages Business Growth – Provides necessary funds for expansion, modernization, and large-scale investments.

- Improves Creditworthiness – Successfully repaying long-term loans builds a strong credit history, increasing future borrowing capacity.

- No Immediate Repayment Pressure – Some long-term loans offer a grace period, allowing businesses or students to establish themselves before repayments begin.

Disadvantages of Long-Term Loans

- Collateral Requirement – Many financial institutions require valuable assets as security, making it difficult for startups to qualify.

- Lengthy Approval Process – Involves extensive documentation, creditworthiness checks, and financial assessments.

- Fixed Repayment Obligation – Businesses must repay the loan even during financial downturns, increasing financial risk.

- Higher Total Interest Payment – Due to the long duration, the total interest paid over time can be substantial.

- Risk of Default and Asset Loss – If a borrower fails to repay, the lender can seize pledged assets.

- Market Risks (for Floating-Rate Loans) – If interest rates increase, repayments can become costlier over time.

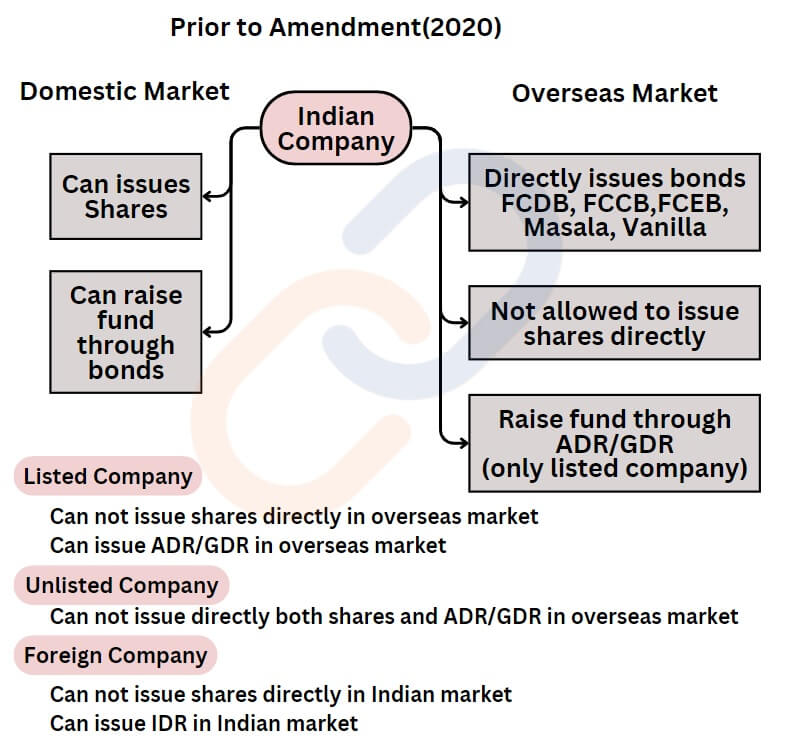

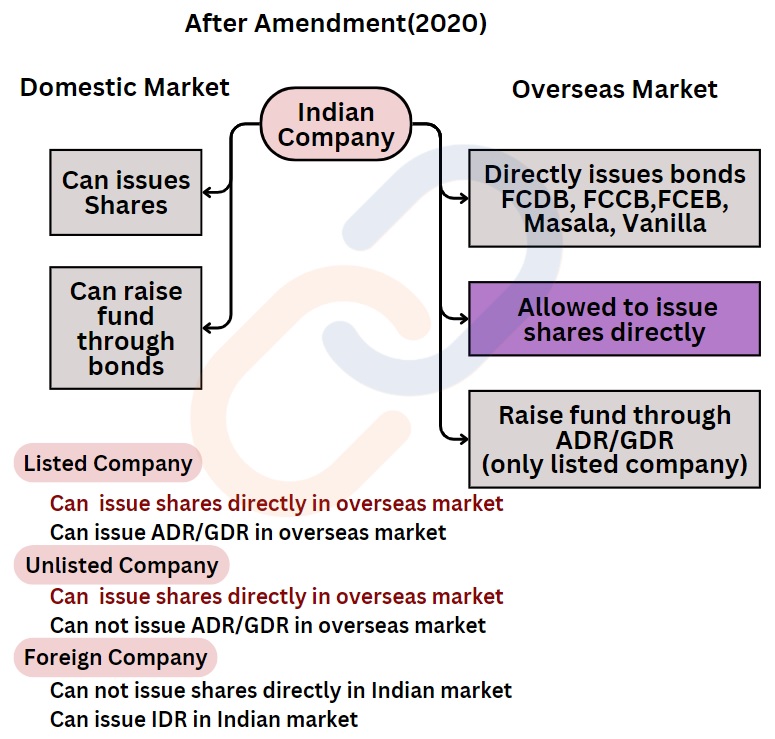

International Financing

The Company (Amendment) Act 2020

- Direct Listing in Foreign Jurisdictions: The Bill empowers the Central government to allow certain classes of Indian public companies to directly list classes of securities in foreign jurisdictions (Foreign Stock Exchange).

- It will help start-ups to tap overseas markets to raise capital.

Scenario before the Company (Amendment) Act 2020

Scenario after the Company (Amendment) Act 2020

International Financing Instruments

Depository Receipts

- The DR is a negotiable certificate issued by a bank representing shares in a foreign company traded on a local stock exchange.

- It comes under Foreign Direct Investment

- Legal framework-

- Depository Receipt Scheme, 2014– formulated on recommendations of the Sahoo Committee

- SEBI Framework for Issuance of Depository Receipts

Example

- Indian Depository Receipts- Foreign companies issue shares through the depository route.

- American Depository Receipts- Indian companies issue shares in the USA through the depository route.

- Global Depository Receipts- These depository receipts are traded in two or more global stock markets.

Foreign Currency-Denominated Bonds(FCDB)

- A foreign bond is issued by an international company in a country different from its own and uses that country’s currency to denominate those bonds.

- Indian companies issue FCDB (in Dollars) in the US market for long-term funds.

- Risk of volatile exchange rate

Plain Vanilla Bonds/ Masala Bonds

- Indian Companies issue Indian currency-denominated bonds in the foreign market for long-term funds.

Foreign Currency Convertible Bonds(FCCB)

- Indian companies issue foreign currency-denominated bonds in foreign markets.

- These bonds are convertible into shares after maturity.

- Risk of volatile exchange rate

- FCCB comes under FDI.

- Example-

- FCCB of Tata Steel issued in the USA converted into shares of Tata Steel.

Foreign Currency Exchangeable Bonds

- Indian companies issue bonds in foreign currency for the long term.

- These bonds are convertible into the shares of other companies of the group.

- FCEB comes under FDI.

- Risk of volatile exchange rate

- Example – FCEB of Tata Steel issued in the USA converted into shares of Tata Motors.

Share issuing in Foreign Market

The Company Amendment Act 2020- Indian companies can issue shares in foreign markets and raise equity capital.