This is Day 19 | 90 Days RAS Mains 2025 Answer Writing, We will cover the whole RAS Mains 2025 with this 90-day answer writing program

Click here for the complete 90 days schedule (English Medium)

Click here for complete 90 days schedule (Hindi Medium)

GS Answer Writing – Elementary knowledge of Government Audit, Basic knowledge of Performance Budgeting, Zero-Base Budgeting । पत्र लेखन

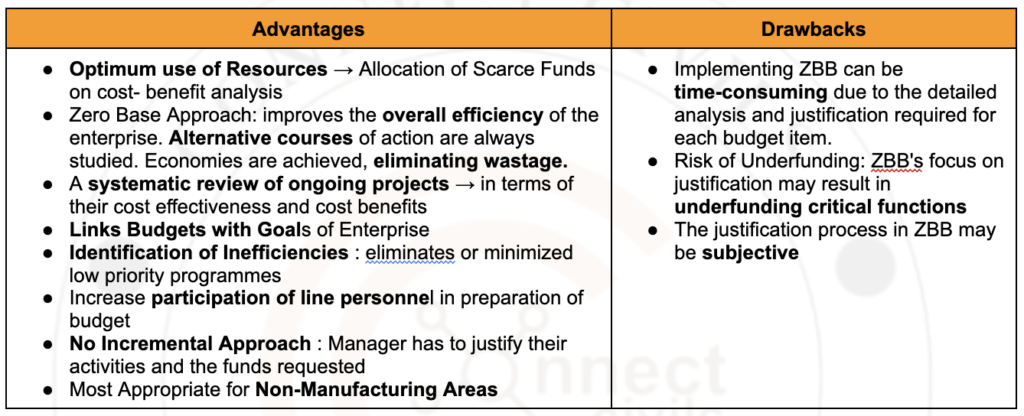

In ZBB, instead of building a budget based on the previous year’s expenditures, every budget cycle starts with a “zero base,” meaning that each expense must be justified from scratch.

In summary, while ZBB offers advantages such as strategic alignment and resource optimization, it may face challenges related to complexity, time consumption, and potential subjectivity. The choice between ZBB and other budgeting methodologies depends on an organization’s specific needs.

Note → In india, ZBB was first introduced in the department of science and technology in 1983 and in all ministries during 1986-1987 Year

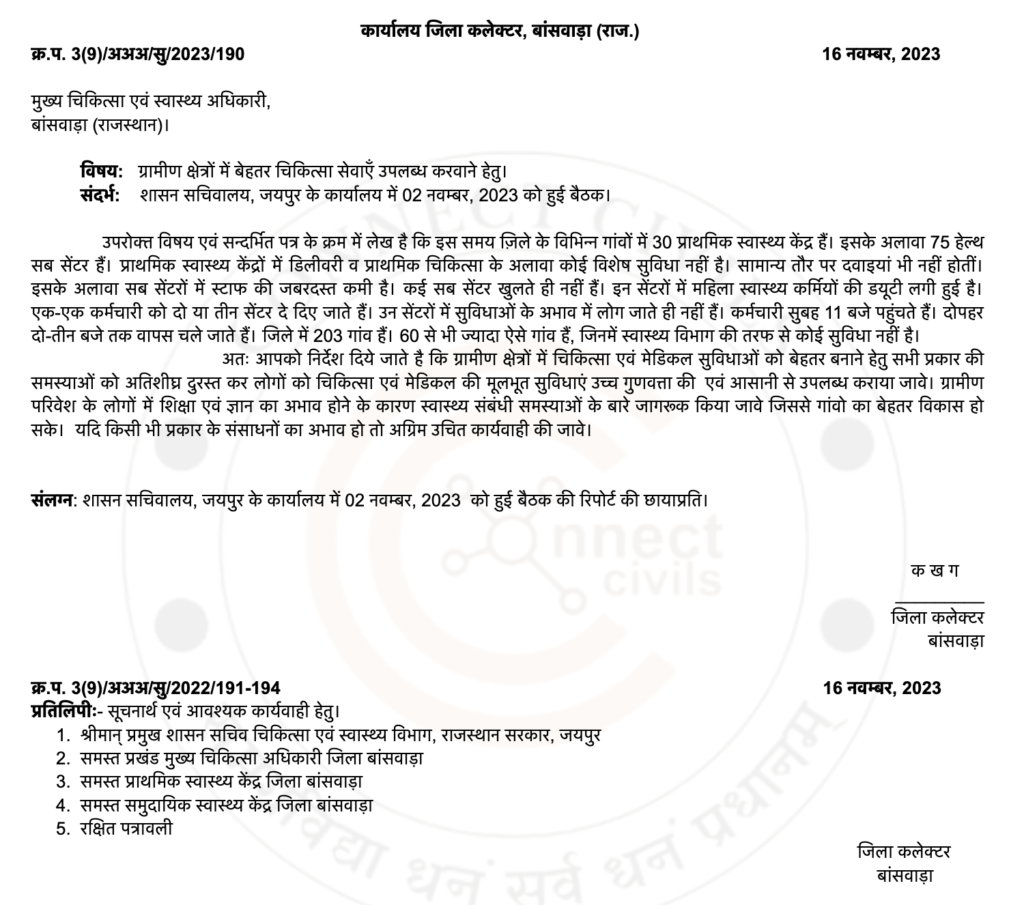

Paper 4 (Comprehension part) – कार्यालयी पत्र

Day 19 | 90 Days RAS Mains 2025 Answer Writing